The RBI’s New Playbook: How Non-Resident Indians Benefit from the Latest Measures

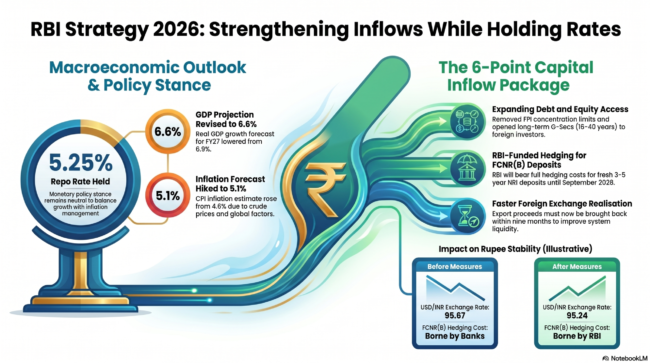

The Reserve Bank of India (RBI) on Friday opted to keep its repo rate unchanged at 5.25% while maintaining a neutral monetary policy stance. However, the central bank unveiled a comprehensive six-point package designed to attract foreign capital and support the Indian rupee. While the measures span various financial markets, Non-Resident Indians (NRIs) and Overseas Citizens of India (OCIs) stand out as major beneficiaries. Through easier stock market access and enhanced foreign currency deposit schemes, the RBI has opened lucrative new avenues for overseas Indians to invest and grow their wealth.

Streamlined Access to India’s Equity Markets One of the most significant changes for NRIs is the introduction of higher investment limits in listed Indian equities. Previously, participating heavily in the Indian stock market often meant navigating traditional Foreign Portfolio Investor (FPI) channels.

Under the new framework, the RBI has extended the facility to invest in listed equities without requiring SEBI registration to all resident individuals living abroad. This pivotal move widens the investor pool, granting NRIs and OCIs far greater flexibility and room to participate directly in India’s equity market growth.

A Safe Haven with Better Returns: FCNR(B) Deposits The RBI is also aggressively courting NRI dollars through Foreign Currency Non-Resident Bank, or FCNR(B), deposits. Unlike standard NRE or NRO accounts which are held in rupees, FCNR(B) deposits are fixed deposits held in foreign currencies such as the US dollar, British pound, euro, yen, Canadian dollar, or Australian dollar. This provides a crucial benefit to NRIs: the money remains in the foreign currency, completely protecting the depositor from the risk of the Indian rupee depreciating.

To boost these inflows, the RBI has announced that it will bear the full hedging cost for banks raising fresh three- to five-year FCNR(B) deposits until September 30, 2026. Hedging acts as “insurance” for Indian banks to protect themselves against currency exchange mismatches if the dollar-rupee exchange rate moves sharply. Because this insurance is typically one of the biggest costs banks face when raising foreign currency funds, the RBI absorbing this expense drastically changes the economics for financial institutions.

As a direct result of these reduced costs, banks are strongly encouraged to offer highly competitive interest rates and attractive terms to NRIs to mobilize their dollar deposits before the September deadline.

For NRIs looking to park their funds in India, the RBI’s latest policies present a rare dual advantage. Investors seeking growth can enjoy expanded access to India’s stock market, while those seeking stability can secure potentially higher returns on risk-free foreign currency deposits.